# Prop Firm Risk Models Explained: How to Trade for Consistency Without Violating Rules

Proprietary trading firms have revolutionized retail trading by providing capital access to skilled traders worldwide. However, their risk management models present unique challenges that many experienced traders struggle to navigate effectively. Understanding these risk frameworks isn't just about avoiding rule violations—it's about optimizing your trading approach to achieve consistent profitability while working within structured parameters.

The sophisticated risk models employed by prop firms serve dual purposes: protecting firm capital while identifying traders capable of generating sustainable returns. For experienced traders accustomed to managing their own risk, adapting to these external constraints requires a fundamental shift in approach, demanding precision in execution and strategic thinking about position sizing, timing, and overall portfolio management.

Table of Contents

- [Understanding Prop Firm Risk Architecture](#understanding-prop-firm-risk-architecture)

- [Daily Loss Management Strategies](#daily-loss-management-strategies)

- [Maximum Drawdown Navigation](#maximum-drawdown-navigation)

- [Position Sizing Optimization Within Constraints](#position-sizing-optimization-within-constraints)

- [Advanced Consistency Models and Scaling](#advanced-consistency-models-and-scaling)

- [Conclusion](#conclusion)

Understanding Prop Firm Risk Architecture

Prop firms implement multi-layered risk frameworks designed to protect capital while allowing profitable traders to scale their operations. These models typically incorporate several key components that work in tandem to create a comprehensive risk management system.

Core Risk Parameters

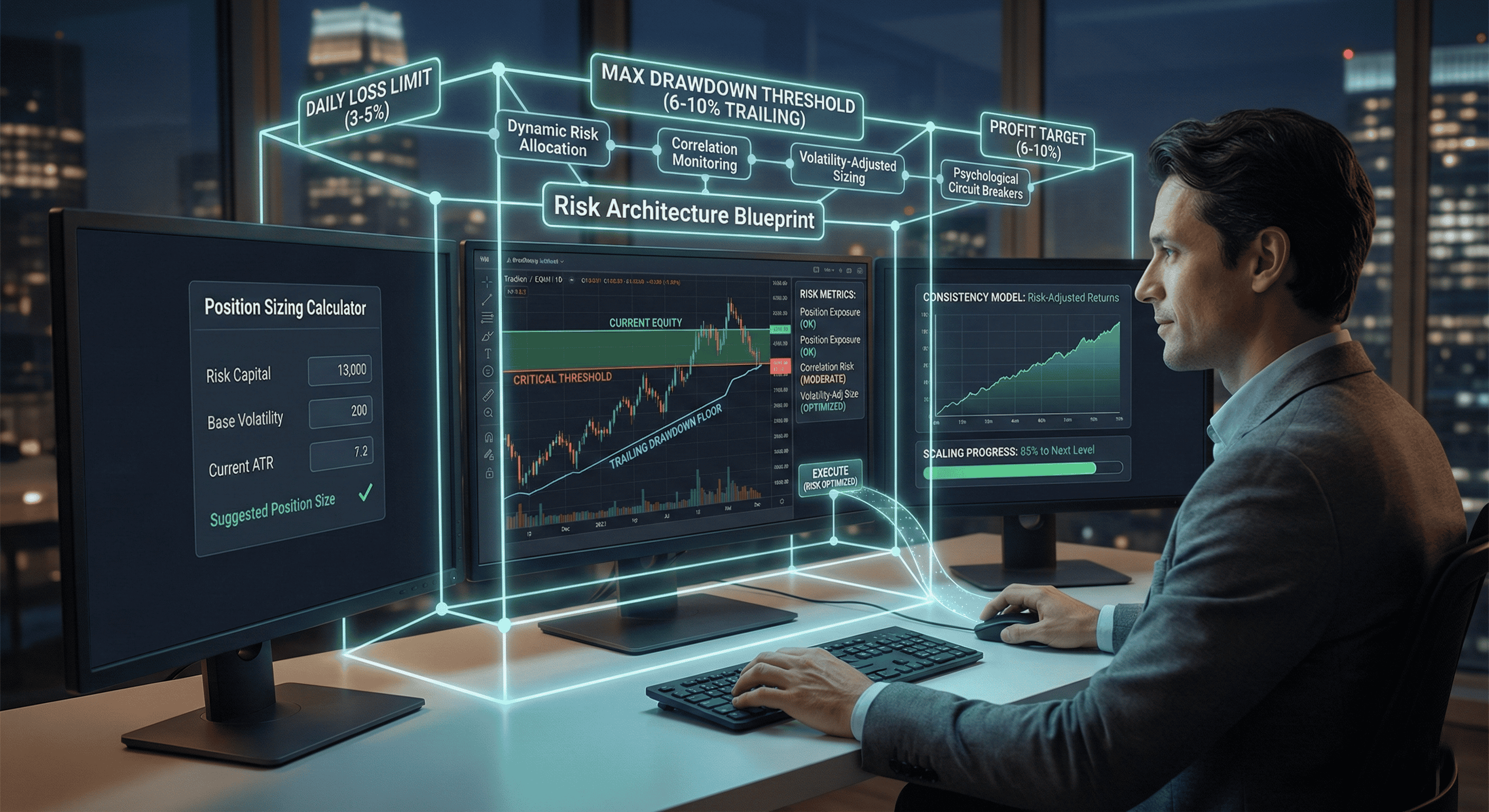

The foundation of prop firm risk models rests on three primary pillars: daily loss limits, maximum drawdown thresholds, and profit targets. Daily loss limits typically range from 3-5% of account equity, creating a hard stop that prevents catastrophic single-day losses. Maximum drawdown limits, usually set between 6-10% from the account high-water mark, ensure that cumulative losses don't exceed acceptable levels.

:::key-concept Prop firm risk models operate on trailing drawdown calculations, meaning your maximum loss threshold moves up with your account as you generate profits, but never moves down when you experience losses. :::

Profit targets serve as the positive reinforcement mechanism, typically requiring 6-10% gains to qualify for account scaling or profit sharing. These targets aren't just benchmarks—they're integral to the firm's assessment of your trading consistency and risk-adjusted returns.

Risk Monitoring Systems

Modern prop firms employ real-time monitoring systems that track multiple risk metrics simultaneously. These systems calculate position exposure, correlation risk, and volatility-adjusted position sizes in real-time, often implementing automatic position reductions or trade restrictions when risk thresholds approach critical levels.

The sophistication of these systems means that traditional risk management approaches may trigger unexpected restrictions. For instance, holding multiple correlated positions during high-volatility periods might result in automatic position sizing reductions, even if individual positions appear within normal parameters.

:::warning Many experienced traders underestimate the sensitivity of prop firm monitoring systems. Correlation calculations often include currency exposure, sector concentration, and volatility clustering effects that may not be immediately apparent. :::

Daily Loss Management Strategies

Effective daily loss management requires a proactive approach that goes beyond simply monitoring P&L. Successful prop firm traders develop systematic approaches to daily risk allocation that account for market conditions, volatility expectations, and their own psychological state.

Dynamic Risk Allocation

Rather than using fixed position sizes throughout the day, advanced traders implement dynamic risk allocation models that adjust exposure based on realized volatility, time of day, and cumulative daily P&L. This approach recognizes that market conditions change throughout the trading session, requiring adaptive position sizing to maintain consistent risk levels.

For example, during the first hour of market open when volatility is typically elevated, experienced traders might reduce their standard position size by 30-50% to account for increased price movement potential. As market conditions stabilize, position sizes can gradually return to normal levels.

:::example A trader with a $100,000 account and 4% daily loss limit might allocate risk as follows:

- Pre-market and first hour: 1.5% maximum risk per trade

- Mid-morning to lunch: 2% maximum risk per trade

- Afternoon session: 1.8% maximum risk per trade

- Final hour: 1% maximum risk per trade

This allocation accounts for typical intraday volatility patterns while maintaining overall daily risk control. :::

Psychological Circuit Breakers

Beyond mechanical stop-losses, successful prop firm traders implement psychological circuit breakers—predetermined rules that force trading cessation under specific conditions. These might include stopping after three consecutive losses, halting trading when daily losses exceed 50% of the maximum allowable limit, or ceasing operations during periods of unusual market stress.

These circuit breakers serve dual purposes: they prevent emotional decision-making that often leads to rule violations, and they preserve capital for subsequent trading opportunities. Many experienced traders find that their best trading days often follow days when they exercised discipline by stopping early.

Intraday Recovery Protocols

When daily losses begin accumulating, having a systematic recovery protocol prevents the desperation trading that often leads to account violations. Advanced traders develop specific strategies for different loss scenarios, including position sizing adjustments, market selection changes, and time-based trading restrictions.

A sophisticated recovery protocol might include scaling down position sizes by 25% after the first 1% daily loss, switching to more liquid markets to reduce execution risk, and implementing tighter stop-losses to prevent further deterioration.

Maximum Drawdown Navigation

Maximum drawdown management represents perhaps the most critical aspect of prop firm trading, as drawdown violations typically result in immediate account termination. Understanding how drawdown calculations work and implementing strategies to navigate these constraints separates successful prop traders from those who struggle with consistency.

Trailing Drawdown Mechanics

Prop firms typically implement trailing drawdown calculations that create a dynamic floor beneath your account equity. As your account grows, this floor rises proportionally, but it never descends when you experience losses. This mechanism means that a $10,000 profit followed by a $6,000 loss doesn't simply result in a $4,000 net gain—it potentially creates a permanent elevation in your drawdown threshold.

:::key-concept Trailing drawdown calculations mean that every dollar of profit you generate becomes part of your permanent risk threshold. A trader who grows a $100,000 account to $110,000 now has an effective account size of $110,000 for drawdown calculations, even if current equity falls back to $105,000. :::

Strategic Profit-Taking Approaches

Understanding trailing drawdown mechanics influences optimal profit-taking strategies. Rather than letting winners run indefinitely, prop firm traders must balance the desire for maximum profits against the reality of permanently elevated risk thresholds. This often means implementing more aggressive profit-taking protocols than might be optimal in personal accounts.

Advanced traders develop tiered profit-taking strategies that secure portions of gains at predetermined levels while allowing remainder positions to capture extended moves. This approach provides protection against drawdown threshold elevation while maintaining upside participation.

Drawdown Recovery Strategies

When approaching maximum drawdown limits, successful traders implement systematic recovery strategies rather than attempting to trade their way out through increased risk-taking. These strategies typically involve:

1. Position Size Reduction: Decreasing standard position sizes by 50-75% to extend trading longevity 2. Market Selection Refinement: Focusing on the most liquid, predictable markets to improve execution quality 3. Time Horizon Adjustment: Shifting to shorter-term strategies with quicker profit realization 4. Correlation Management: Eliminating correlated positions to reduce portfolio-wide risk

:::tip Many successful prop firm traders establish "safety zones" at 70-80% of maximum drawdown limits, implementing enhanced risk protocols before reaching critical thresholds. This proactive approach provides additional buffer room for recovery efforts. :::

Position Sizing Optimization Within Constraints

Effective position sizing within prop firm constraints requires sophisticated approaches that balance profit maximization with rule compliance. Traditional position sizing methods often prove inadequate when working within external risk parameters, necessitating more nuanced approaches.

Multi-Constraint Optimization

Prop firm traders must simultaneously optimize for multiple constraints: daily loss limits, maximum drawdown thresholds, profit targets, and often additional parameters like maximum position size or correlation limits. This multi-constraint environment requires position sizing algorithms that can balance competing objectives.

Advanced traders employ position sizing models that consider the interaction between these constraints. For example, when approaching daily loss limits, position sizes might be reduced not just to prevent violations, but to preserve optimal positioning for subsequent trading opportunities.

Volatility-Adjusted Sizing

Traditional fixed-dollar or fixed-percentage position sizing proves suboptimal in prop firm environments where risk parameters remain constant while market volatility fluctuates significantly. Sophisticated traders implement volatility-adjusted position sizing that maintains consistent risk levels across varying market conditions.

This approach involves calculating position sizes based on recent volatility measures, typically using Average True Range (ATR) or standard deviation calculations to normalize risk across different market conditions and instruments.

:::example A volatility-adjusted position sizing formula might look like:

Position Size = (Risk Capital × Base Volatility) / (Current ATR × Price)

Where:

- Risk Capital = Maximum acceptable loss per trade

- Base Volatility = Historical average ATR for normalization

- Current ATR = Recent volatility measure

- Price = Current market price

This formula automatically reduces position sizes during high-volatility periods and increases them during low-volatility conditions, maintaining consistent risk exposure. :::

Correlation-Aware Position Sizing

Prop firms often monitor portfolio-level correlation risk, requiring traders to consider how individual positions interact within their overall portfolio. Advanced position sizing approaches account for these correlations, reducing individual position sizes when holding multiple correlated instruments.

This correlation-aware approach might involve reducing standard position sizes by 20-30% when holding positions in closely related instruments, or implementing maximum exposure limits across correlated asset classes.

Advanced Consistency Models and Scaling

Prop firms evaluate trader performance using sophisticated consistency models that go beyond simple profit and loss calculations. Understanding these models and optimizing performance within their parameters is crucial for long-term success and account scaling.

Consistency Metrics and Evaluation

Modern prop firms employ multiple consistency metrics including profit factor ratios, maximum consecutive losses, daily profit standard deviations, and risk-adjusted return measures. These metrics collectively paint a picture of trader reliability and skill level.

Successful prop firm traders optimize their trading approaches to perform well across all evaluation dimensions, not just raw profitability. This might involve accepting slightly lower overall returns in exchange for more consistent daily performance, or implementing strategies that specifically target improved profit factors.

:::key-concept Prop firms typically weight consistency metrics heavily in scaling decisions. A trader generating 15% returns with high volatility may receive less favorable scaling terms than a trader generating 12% returns with low volatility and consistent performance. :::

Scaling Preparation Strategies

Preparing for account scaling requires strategic thinking about how trading approaches will adapt to larger capital allocations. Many strategies that work effectively with smaller accounts face liquidity or execution challenges when scaled to larger sizes.

Advanced traders begin preparing for scaling early in their prop firm journey by:

1. Market Selection Optimization: Focusing on liquid instruments that can accommodate larger position sizes 2. Execution Strategy Development: Implementing advanced order types and execution algorithms 3. Strategy Diversification: Developing multiple uncorrelated approaches to reduce concentration risk 4. Technology Infrastructure: Ensuring trading platforms and internet connectivity can handle increased activity

Performance Attribution Analysis

Successful prop firm traders conduct regular performance attribution analysis to understand the sources of their returns and identify areas for improvement. This analysis goes beyond simple win/loss ratios to examine factors like time-of-day performance, market condition sensitivity, and strategy-specific results.

This analytical approach enables continuous improvement and helps identify potential issues before they impact overall performance. Traders might discover, for example, that their afternoon trading performance consistently underperforms, leading to strategic adjustments in daily trading schedules.

:::tip Maintain detailed trading logs that capture not just execution details but also market conditions, emotional state, and decision-making rationale. This information proves invaluable for performance attribution analysis and continuous improvement efforts. :::

Risk-Adjusted Performance Optimization

Prop firms increasingly focus on risk-adjusted performance metrics rather than absolute returns. Successful traders optimize their approaches to maximize metrics like Sharpe ratios, Calmar ratios, and other risk-adjusted measures.

This optimization often involves accepting lower maximum returns in exchange for reduced volatility, implementing more sophisticated risk management techniques, and developing strategies specifically designed to generate consistent, risk-adjusted returns rather than maximum profits.

Conclusion

Mastering prop firm risk models requires a fundamental shift from traditional retail trading approaches. Success demands sophisticated understanding of multi-layered risk constraints, implementation of advanced position sizing methodologies, and development of systematic approaches to consistency optimization.

The most successful prop firm traders view these constraints not as limitations but as frameworks that force discipline and consistency—qualities that ultimately enhance long-term trading performance. By developing systematic approaches to daily loss management, implementing sophisticated drawdown navigation strategies, and optimizing position sizing for multi-constraint environments, experienced traders can thrive within prop firm structures while building scalable trading operations.

The path to prop firm success lies in embracing these risk models as tools for improvement rather than obstacles to profitability. Traders who master these systems often find that the discipline and consistency required for prop firm success translates into improved performance across all trading activities.

Ready to apply these advanced prop firm strategies to your trading? Start by analyzing your current approach against the risk model frameworks discussed here, identifying areas where systematic improvements can enhance both compliance and profitability. Remember, success in prop firm trading isn't just about avoiding violations—it's about building sustainable, scalable trading operations that generate consistent risk-adjusted returns.